Do you have a detailed personal budget?

Do you hate the thought of tracking every single penny?

Well me neither and me too.

And yet, I do have a good picture of how much I’m spending in my broad categories. More importantly, I have clear confidence that I can do whatever I want with the money available on my credit card, and I can still pay my bills, have food on the table, and have a buffer of cash for emergencies and large purchases.

I don’t need to track every receipt and every expense. I don’t have to worry about my spouse splurging on something that might endanger our bills.

Sounds too good to be true?

I’ll show you how to do it.

This is my personal cash flow system. A set of cascading buffers if you will, that makes sure that there is money for the things I need when I need them, I know where the money is going, but I still don’t need to keep track of every small purchase.

Go ahead and track every single penny if you want. It’s a great exercise to do and you get good insights from it. If money is really tight, it might also be a necessity so you can identify places to cut down.

But I argue that it’s not strictly necessary in order to keep a sense of comfort and security that you know what’s going on.

It started with a simple version of the system that worked for me as a single household, and then evolved slightly to what we have to day with a family of four.

Why would you want to have a system?

When I was in my early twenties I got accepted to a university programme. I was very happy and looked forward to it a ton. But it also scared the living shit out of me because I now had to live on student loans.

Now why would I be scared? Going straight from high school to university student isn’t usually this kind of scary. Perhaps it would be your first time handling your own finances as an adult and actually be an upgrade from having very little money at all.

But I had already been working full time for 2 years before this, which meant that I had gotten used to living on a regular paycheck. I had already moved away from home, living in my own apartment with utilities and rent and all kind of expenses.

The thought of making do on student loans was frightening to say the least. I didn’t trust myself to not spend all the money I had in my bank account and have money left at the end of the month for bills.

How was I going to be able to make ends meet and stay in my flat when my income would drop by almost 40%?

So I created a system to protect me from myself. With small tweaks and additions over the years, I am actually using the very same system today. It has been working for me for over 15 years.

Ready? Here goes…

The TL;DR

In essence, the system can be summarised as:

- Keep the money for your regular expenses and bills separate from your credit card.

- Transfer money monthly for food and groceries to a store debit card (or another debit card).

- Give yourself a monthly allowance for discretionary spending. This is what your credit card has access to.

- Include savings as one of your regular expenses. Treat it as a bill.

- Catch any overflow and steer towards a rainy day fund. After rainy day fund, begin investing.

What you need

The basis of this system is having several bank accounts. Here in Sweden, having online banking also gives you the possibility to create a small number of bank accounts for free. No extra charge. What they charge you for is your credit card, basically. (And while I will continue to write “credit card” in this article, my card is in reality a debit card. Also a legacy from my time as a student, where I did not want to put myself in debt under any circumstances)

Setup a separate bank account for your big categories

- Your main account, where money comes in and get automatically transferred and withdrawn from

- Your spending account, that your credit card has access too

- One savings account for larger planned purchases

- One savings account for your rainy day fund

Optionally add

- A car/vehicle account

- A food and groceries account, with a separate credit card (if you don’t want a store card)

- A house account for house owners’ maintenance and repairs

I guess my system is a kind of a digital version of the envelope system for budgeting, except that I’m not necessarily so strict on not redistributing funds if I get a category estimation wrong.

The big premise is perhaps the less intuitive choice – your credit card is not attached to the same bank account that pays the bills.

I’ll say that again:

Do not attach your credit card to the same bank account that pays the bills.

I’ll address the situation with credit card subscriptions further down.

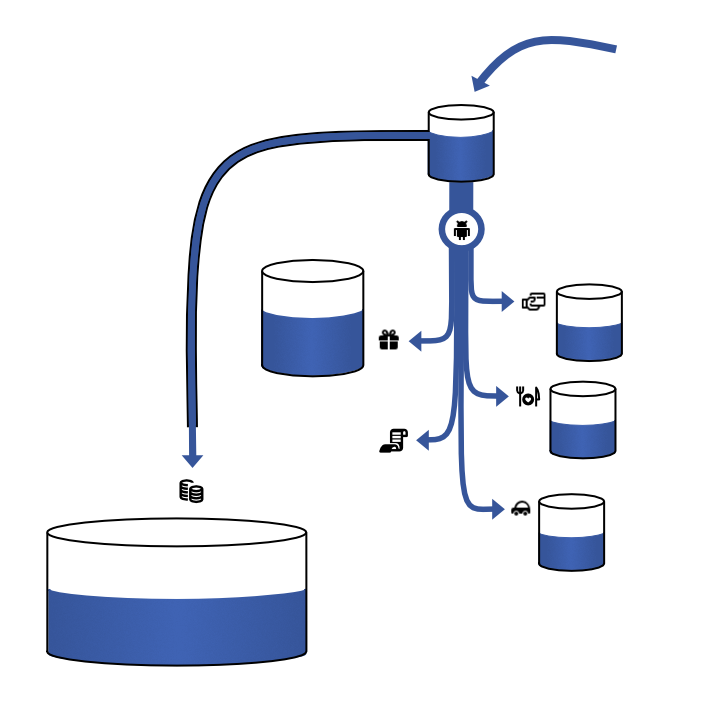

Here’s what I did from the start:

Money came in to my main account. From there I

- Transferred grocery money to a grocery store debit top-up card

- Transferred money for the regular expenses to a bill-paying account

- Utilities

- Rent

- Other regular expenses, like memberships etc

- Transferred a little bit to a savings account for bigger purchases

- Kept discretionary spending on my credit card account. Whatever was left over after all the transfers was free for me to spend.

As a student, my main concern was being able to stay in my flat and keep food in my belly. I transferred expenses and food money to a safe place and then the rest was coffee, entertainment and the like. I had no other things I needed to think about. Ah, the simple times.

Later on, I switched the card connection, so the main account where money comes in would be the account from which I paid the bills. I also added a separate bank account for the car expenses to which both me and my spouse contribute.

So my current system looks like this

Money comes in to the main account. From there:

- Transfer monthly grocery money to a grocery store debit card

- Transfer a monthly allowance for discretionary spending to the credit card account

- Transfer monthly car money to the car account

- Leave enough in the bill paying account for the recurring expenses, and a buffer of about one month’s worth. Saving is treated as part of your regular expenses.

- Transfer any excess money to the rainy day fund

And voilà – you now know that

- You have money for food for the rest of the month

- You’ll be able to pay the bills when they come

- You have put away something towards savings and larger expenses

- All money available to you on the credit card are OK to spend on whatever you want.

Put it on autopilot

If these transfers seem like a lot to remember, don’t worry. Most of these are put on autopilot using recurring automatic wire transfers.

Employees are typically paid once a month here in Sweden, and I created monthly transfers due a couple of days after payday. If you are used to being paid twice per month, just divide your monthly transfers in two.

And if you are a business owner, give yourself a regular paycheck and this system will work for you too. You should already be separating your personal money from the business money anyway. Just make sure that the paycheck you give yourself is after-tax-money, and reserve enough for taxes on the business side.

Only track what’s necessary

So how do you know how much to put in these categories? Well there is a little bit of tracking going on, I admit that.

I treat budgeting just like time tracking. I don’t track every last penny all the time, just like I don’t track every second of my day all the time. But occasionally it can be a good thing to do to calibrate the system.

Depending on your personality, you can decide in which end to start. You might want to start by tracking one month’s expenses and then use that as a base for your monthly transfers.

But a budget is nothing but more or less well educated guess anyway. If you hate the thought of doing detailed tracking for a full month and have no idea of how much you spend in a month – make a guess!

If you guess too low one month, make a note of it and transfer a bit more next month. If you guess too high, just lower the amount next month.

The tighter your finances are, the more important it is that you make accurate guesses. So if you’re in financial scarcity right now, you will need to do some gathering of data in order to make good predictions before setting this up.

But the only place where you need to sit down and make some calculations in the beginning is your regular expenses, like your bills. You probably also need to sit down and calculate how much to allocate to the vehicle and house account each month if you have those.

Savings are non-negotiable

How much to put in savings? Some people say to save 10% of your income but I auto-save a fixed amount every month. This will all depend on your circumstances of course.

During my roughest years, 10% would have been an impossible target and I saved the equivalent of $50/month (which still hurt a bit). But this is a non-negotiable. Always always put something into your savings account each month.

If you have a specific thing you want to buy, divide the price with the number of months you want to save to get an amount. Or divide the price with the amount you can save per month to find out how long you have to wait in order to afford it.

Either way, tack on that amount to your savings transfer or make a new auto-transfer for this specific savings target. New MacBook Pro every 3-4 years? That’s about $65-$80/month.

Buffering the cash flow

The biggest thing I feared when I created the system was the fact that some bills come irregularly. At that time, I think it was my electricity that was billed every quarter.

This would mean that those months, I’d have to cough up the equivalent of an extra $75. That was like a whole week’s worth of food at the time and when margins are tight, these things can break you.

So I divided up my expenses to monthly charges instead. By setting aside $25/month towards the bill account for electricity, I had enough cash on hand to pay the electricity bill when it came. A yearly membership of $30? That’s $2,5/month.

I gathered all my regular bills and expenses for one year, and divided that by twelve to get the monthly expense transfer needed.

Today I have a bit of leeway regarding cash flow through buffering.

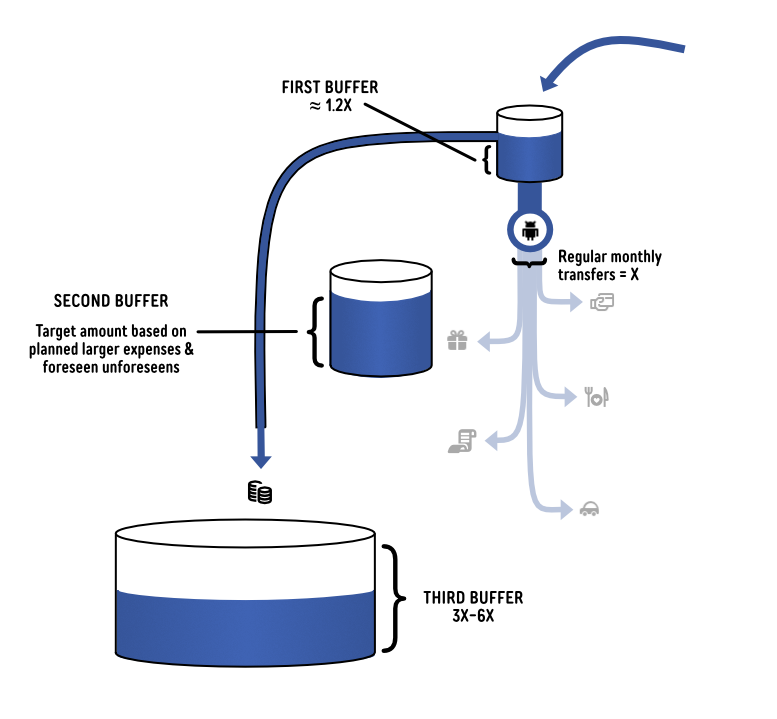

Triple buffers

My system means I have three buffers of increasing size. The first buffer is in the monthly expense account, a bit more than one month’s total expenses after all the main bills are paid and all transfers completed.

This means I’m no longer sensitive to smaller fluctuations in recurring charges and expenses. The idea is also that if for some reason my income is delayed, all the bills that are on autopilot can still get withdrawn without going into overdraft.

The second buffer is my standard savings account. For the larger infrequent expenses. I haven’t calculated a finite size for this, but you’d want to have minimum double or triple the cost of replacing any large appliance or expensive item that can break.

You want to be covered if both your computer and your washing machine breaks down in the same month. Add also any deductible for your insurances to you know you are covered if you’d need it.

The third buffer is my rainy day fund, from which I refill the main account when other parts of the system is running dry.

What do you need to track then?

You need to gather enough data to be able to evaluate your guesses.

I keep a spreadsheet where I have one sheet for our monthly bills and one sheet for the car expenses. I update it once a month as the bills get paid, simply entering what I was paying that month. It’s not a lot of work at all.

By the end of the year, I can see the average expenses per month and re-calculate my guesses towards the next year. This also means I update my buffer targets to reflect my monthly expenses.

The credit card subscriptions

So what about all those subscriptions you have tied to your credit card? Are they not bills?

Well yes of course. 15 years ago this was not an issue but these days, I too have a number of regular expenses that are charged to my card.

You have two options. One is to include those subscriptions in your monthly allowance. You will then need to remember not to spend that money so there is a balance on your card when they try to charge you.

Or, include it in your monthly recurring expenses and setup a monthly wire transfer from your bill account to the credit card account. It’s very easy to do in my online bank, and I guess it is for you too. Set it and forget it. Just make sure to set the transfer date to a couple of days before the charge is due to account for weekend/transfer time.

Benefits of using this system

Peace of mind

This benefit is the biggest one. If you only take one thing away from this, then physically separate your regular expenses from your discretionary spending because of the peace of mind it gives you.

I don’t have to track how much money I need to mentally reserve on my account for bills. I don’t need to worry about if a splurge will not make ends meet this month.

Knowing that I will still have money to pay the bills and keep a roof over my head, no matter how much money I spend using my card is great.

Having cash on hand for large purchases

The first place I dip into if there’s something I need to buy that doesn’t fit in my allowance is the bill-paying account. Having a month’s worth of expenses there means that a smaller withdrawal from there won’t make a big difference. It’ll get refilled next month.

But for larger planned (and unplanned) purchases, I use the second buffer and simply transfer money from the savings account to the credit card account when I need to.

New laptop? New furniture? I know I’m covered.

Freedom to splurge

The most obvious benefit is of course that you have the freedom to spend the money on your credit card as you like.

New clothes? A fun toy for the kids? A tech gadget? A bottle of fine wine?

If I can fit any purchase within my allowance, I don’t have to think twice about it. No guilt. No worry.

Friction gives protection from impulse buys

If there is something I want to purchase that is outside of discretionary, I need to transfer money from another account. Either the bill paying account (first buffer) or the savings account (second buffer).

This is a good thing in my view.

It requires me to think twice about my investments and reduces impulse buys. The friction is small these days because of online banking anyway, but having this small barrier there is beneficial.

Damage control protection from credit card fraud

Another benefit is that if my card gets stolen, lost or skimmed, all I’m losing is my discretionary spending. The criminals have no access to my savings, my bills will still get paid and we will still be able to eat this month. (And since it’s a debit card, they can’t put me in debt either). That is also peace of mind.

When you start to get more money than you need, I still suggest to keep having a monthly allowance. Increase it if you like. But keep it.

Use the overflow to build your rainy day fund, and keep that small barrier of transferring money for large purchases. Even if you can afford the purchase per se, it’s still good to stop and think and reflect on why you want to bring that item into your life.

In fact, I think this little friction to the impulse shopping is more important for those who have a lot of money than those who don’t. It easier to buy without thinking when money is not a problem.

There’s always money for food and groceries

Having a separate food account is a more optional part of the system. When we had a more positive cash flow, we didn’t always do this. You can simply increase your monthly allowance to include groceries if you know that you have enough to go around.

Having a separate account for food (and other household items) becomes more beneficial the tighter your margins.

Anyone in the household can do the grocery shopping

Having a separate grocery card is also beneficial when the one who is bringing in the cash is not the one doing most of the shopping. By having a separate food account, these things don’t matter.

Both me and my husband have had periods where the income has fluctuated and one has been earning more than the other. In those times, we have not always contributed equally to the food account. Sometimes one person was responsible for it all (and bills too).

But we both have separate cards with access to this joint account. So it doesn’t matter who is doing the shopping, the money comes from the same place.

An added benefit is also that most store chains have some kind of loyalty program, so it’s also possible to save some money by choosing a single provider.

The car expenses are shared and prepaid

This setup is the same as the separate food account, really. The difference here is that our car account is a bank account only without a card attached, and instead need money transfers whenever we pay for something regarding the car.

But I think the benefits outweighs the slight hassle. It doesn’t matter which one of us is filling up gas in the car, the money gets transferred from the car account to the person who paid.

When it’s time for car service or some kind of repair, it doesn’t affect our monthly cash flow. There’s already money reserved for that in the car account.

Of course, things can happen that have not been planned for. We will probably need to change the gear box next year, and that will be a bigger expense than I have previously accounted for in our monthly transfers. We’ll might need to dip into savings for that, or temporarily increase the monthly transfers for a while.

But in general, this system works very well. I recalibrate the monthly transfers at the end of the year, where I compare what I thought we would spend with what we actually spent. And adjust for increased gas prices etc.

Something I also included in the monthly car allowance was of course payment of the car loan. While this debt was paid off last summer, we haven’t decreased the monthly transfer at all.

This means we are putting away money in advance for a new car, so we hopefully will be able to pay for it in cash when the day comes. At the very least it will cover a good chunk of it.

Building up a rainy day fund

I don’t think I need to sell you on the benefits of a rainy day fund. Everyone talks about having it. This is a common advice but few people actually get there.

To be specific, it’s a liquid buffer of a couple of months’ expenses. By liquid I mean cash available on bank account, and not bound in stocks or index funds or anything like that.

How many months to aim for depends on your life situation and risk tolerance. Somewhere around 3–6 months is a good target, a risk-taking entrepreneur providing for a family might prefer 9-12 months to counter unpredictable cash flows.

What this system gives you is that you now have a very easy way to calculate the buffer you want to aim for.

Regular monthly bills + savings + monthly allowance + monthly food transfer + monthly car transfer = one month’s total expenses

For a family with joint finances, include spouse’s expenses+allowance too.

Easing out cash flow issues

Over the years, I’ve had several periods when money did not flow in regularly. I’m sure any business owner can relate to this.

But this has also happened when I’ve had to wait for unemployment benefits, or money from health insurance or parental benefits. I knew the money would come, but they were stuck in the bureaucratic machinery.

I have then transferred money from the rainy day fund into my main account, just as if I gave myself a paycheck.

All my automatic transfers have then kicked in just as normal, no overdrafts anywhere. And when I finally received the money, I sent them back to the rainy day fund again.

Having a back-up for rough times

While our rainy day stash wasn’t fully funded when I burnt out, it has supported me well during my recovery. I was living completely on health insurance for a year, and partially so for 9 more months after.

Thanks to this buffer, we have been able to provide for the kids without worrying too much. Yes our standard of living has been lowered, but I have regularly used money from the rainy day fund to pad things up where needed and keep everything afloat.

Now that I’m back on my feet, I’m tightening my discretionary spending a bit so I can focus on rebuilding this buffer.

Flexing the system for lush and lean times

When money is flowing

When more money is coming in than you need to live on – great! Go ahead and pad the transfers for Food and Discretionary money.

Like I said, when I first moved in with my husband we ditched the separate debit card for groceries all together. At that time we could just buy all the food we wanted and not worry about it. Two incomes, no kids.

Later on, the grocery card got reintroduced again. Partly this was convenience. And even later on we needed it when we started a family and finances became tighter.

You too could simply include food expenses in your monthly allowance, but I suggest you keep them separate. If only because it gives a good lazy overview of what you spend where, without having to track receipts.

Catch the overflow

The huge benefit of this system is how easy it is to catch the overflow.

When you have all the buckets you need for a comfy living filled to the brim, then all the overflow can go towards building a rainy day fund.

Got the rainy day fund covered? Well once you’ve filled that buffer up, the remaining overflow goes towards investing. That’s beyond the scope of this article, but the idea is that the money you invest is money you can afford to lose.

If your rainy day fund can catch you when you fall, then go ahead and invest in those cryptocurrencies!

When money is tight

When money is tight, that’s when you can start to zoom in and track each category in more detail.

I’m not going to talk about all the money saving tricks in the world, but show you how this system adapts to a tighter money flow.

Shrink your discretionary spending

Fun money is the obvious place to start cutting back. Since it is for pure enjoyment it’s not strictly necessary for survival.

Start by simply lowering your own monthly allowance and see how you manage. If needed, calculate what kind of minimum discretionary spending you can live with and only transfer that.

Don’t eliminate this category completely! It will only make you feel deprived and depressed. If you can’t afford going to coffee shops a lot but love coffee, keeping the ability to treat yourself to that double latte once a week – or even once a month – can make wonders for your quality of life.

Tighten the food budget

Food is of course also a place that you can leverage a lot. All the classics of buying in bulk, packing lunchboxes, choosing cheaper alternatives etc.

This category works less well with starting by lowering the monthly amount. Instead start by changing some habits and see how much money you have left over by the end of the month. Then, decrease the monthly food transfer by that amount.

The other option is to go bottom up – to sit down and really calculate how little you can get by with. Plan your meals, add up the costs and make that your new monthly food transfer.

Re-evaluate all regular expenses

It’s also time to take a hard look at those regular bills. Cancel subscriptions you don’t need. Renegotiate terms on others, change providers or downgrade to cheaper plans.

But keep paying yourself too. I always, always put the equivalent of $50 in my savings account. This is actually more important than ever when money is tight.

You can’t use some of your discretionary spending when something comes up because there’s just not enough of it! Your savings account will be the place to go that can save you from going in to debt when you suddenly need to replace something that’s broken.

Drawbacks of the system – none?

I haven’t found many drawbacks to this system. It has worked very well for me for over 15 years so I guess I have gotten so used to the negatives that if they exist I’m not aware of them. 🙂

One thing is that having a debit card attached to a specific chain of stores ties you to shop at that chain. I am not really extremely loyal towards our chain, it just happens to be the shops closest to us so we would probably buy there anyway.

An option if it bothers you to be tied to a chain is to create a separate joint bank account with one card each for you and your spouse. Make it a debit card and not credit card. Now you have the same benefit but with more freedom of choice.

We have actually begun talking of doing exactly this because we want the flexibility of not being tied to a specific chain of stores. But this system has served us so well that I’d rather pay for another debit card in order to keep the system going.

As you can see, me and my spouse have separate finances. We share our shared expenses, but manage our own incomes.

But I know this system would work for a sole family provider too because we have had periods in the past where one of us was the only one earning money. In any case, I think it’s important that both parties at least have separate discretionary money that they can do whatever they want with.

Acknowledgements

I have been through both rough times and flush times with this system, so I know that it works in many circumstances. Or at least it has worked for me.

For a while, I was closely following the blog The Simple Dollar and working hard on living frugal and making every penny count. Now most of my system is set on autopilot and I am no longer into the frugal community. I’d rather work on increasing the money that comes in rather than pinching every single penny that comes out.

This whole write up was inspired by Tiago Forte’s post about the Parallels Between Money and Productivity (membership required) where he compares notes from the book You Need A Budget with a personal productivity mindset.

I have not read You Need A Budget nor used the services, but I’ve heard of it. Now that I got to read more about it, it seems like they and I have come to similar conclusions with similar principles – albeit with slightly different tactics and tools.

Likewise I just began reading Profit First, which also seem to use a similar setup with several accounts for your main categories for your business. It will be interesting to compare the results and see if there’s anything I’d like to tweak.

If this was helpful to you, and if you decide to implement anything from this system, do let me know! I’d love to hear your thoughts.